Some EU steelmakers have been arguing that the free allocation phase-out under the EU Emissions Trading System (ETS) should be slowed down, as they fear the scheme may negatively affect their competitiveness. While some European steelmakers who have invested in decarbonization are asking to save the ambition of the ETS [1], others claim that any efforts on their part would have no business case without the extension of free allocation beyond 2034, or some financial support [2].

We show here that these claims are unfounded and that, on the contrary, EU steelmakers will greatly benefit from the EU’s carbon market and its Carbon Border Adjustment Mechanism (CBAM).

ETS benchmarks until 2030: all carrots, no sticks

Free allocation to the steel sector is very generous: Art. 10a(2)(e) of the ETS Directive granted a near freeze to the hot metal benchmark, rewarding primary ironmaking until at least 2030. The 2024 reform of the Free Allocation Regulation further extended this benchmark to the production of direct reduced iron (DRI), which has much lower emissions (0.39 tCO2/t in the EU, according to the JRC [3], compared to 1.248 EUA for the benchmark) creating windfall profits of 0.858 EUA per tonne of DRI produced.

The proposed EAF carbon steel and EAF high alloy steel benchmarks will lead to a nearly three-fold increase in free allocation to electric arc furnaces compared to the 2021-25 period. This is because in 2021-25, the value of these benchmarks included indirect emissions, even though the actual allocation was only based on direct emissions. This exception concerned 14 benchmarks under the regime of “exchangeability of fuel”. Because this regime was abolished in 2024, free allocation has been directly linked to the benchmarks since the beginning of 2026. However, the values of the benchmarks were still calculated based on both direct and indirect emissions, resulting in a big increase in free allocation, creating more windfall profits.

Furthermore, EU steelmakers, especially operators of electric arc furnaces and electrolytic hydrogen producers, also receive indirect carbon cost compensation (ICC). This can also create over-compensation, because the calculation of ICC can be done based on the assumption of 100% fossil electricity, whereas power prices often fall well below fossil generation costs, including to negative levels.

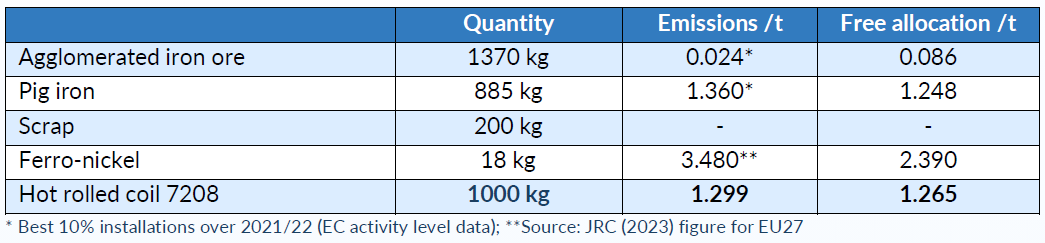

In parallel with changes linked to the newly proposed benchmarks, free allocation is set to decrease over time due to the ramping up of the CBAM. It is therefore necessary to distinguish between the effect of the benchmarks and the effect of the CBAM. Without the CBAM, steel producers that would continue to not decarbonise could be reassured: for such producers, ETS costs would remain extremely low for another five years. Table 1 shows the amount of emissions and free allocation earned by a typical blast furnace / converter plant for 1 tonne of steel. The difference between the two is 0.035 EUA, i.e. €2.72 at today’s price.

Table 1: Emissions vs. free allocation for 1 tonne of blast furnace steel, without CBAM

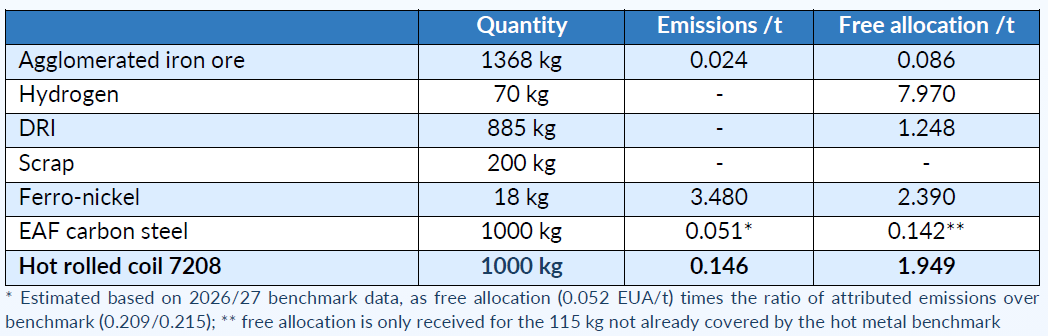

On the other hand, steelmakers opting for greener steel production would greatly benefit from the proposed benchmarks in 2026-30. As calculated in Table 2, the difference between the free allocation received and the emissions would provide 1.802 EUA (€144) per tonne of steel, equivalent to a 25% premium over the market price (about €600 a tonne) of ordinary steel HRC.

Table 2: Emissions vs. free allocation for 1 tonne of HRC steel produced from electrolytic hydrogen DRI

The CBAM effect

Costs tor EU installations

As mentioned above, free allocation for steelmakers will gradually decrease as a result of the CBAM’s introduction.

For EU producers, free allocation will be reduced as a result of the CBAM by 2.5% in 2026 and by 5% in 2027. For 1 tonne of steel HRC, this reduces revenues by the following amount:

Lost revenue (2026) = 2.5% x (free allocation without CBAM: 1.265) x (EUA price: €75.36) = €2.38

Lost revenue (2027) = 5% x 1.265 x 75.36 = €4.77

Lost revenue (2028) = 5% x 1.265 x 75.36 = €9.54

Costs for third-country imports

For importers, CBAM compliance costs are given by the following expression:

CBAM Cost = (Embedded emissions – SEFA) × EU ETS price [4]

Where SEFA stands for “specific embedded free allocation” and is 97.5% of the product’s CBAM benchmark in 2026, 95% in 2027, and 90% in 2028. CBAM benchmarks are set in Implementing Regulation 2025/2620. For 1 tonne of steel HRC made from the blast furnace + converter route, the CBAM benchmark is 1.370 tCO2e if emissions are reported as default values, or 1.168 tCO2e if using actual data with the precursors listed in Table 1.

Embedded emissions can be reported by using either actual data or default values. In a 2023 study, the JRC estimated that actual CBAM-covered emissions for Chinese HRC steel was 1.84 tCO2 per tonne. In contrast, default values are set by Implementing Regulation 2025/2621 and the default value for Chinese HRC is 3.169. A mark-up of 10% is applied to the default values in 2026, 20% in 2027, and 30% from 2028.

For 1 tonne of steel Chinese HRC, the cost of CBAM certificates can therefore be estimated as follows.

If using actual data:

CBAM fees (2026) = (1.84 – (97.5% x 1.168)) x 75.36 = €52.8

CBAM fees (2027) = (1.84 – (95% x 1.168)) x 75.36 = €55.0

CBAM fees (2028) = (1.84 – (90% x 1.168)) x 75.36 = €59.4

If using default values:

CBAM fees (2026) = (3.169 x 1.1 – (97.5% x 1.370)) x 75.36 = €162

CBAM fees (2027) = (3.169 x 1.2 – (95% x 1.370)) x 75.36 = €188

CBAM fees (2028) = (3.169 x 1.3 – (90% x 1.370)) x 75.36 = €218

Costs for lower-carbon imports

Since the CBAM is a tax on carbon intensive goods, we have also calculated CBAM costs for steel HRC produced from a less carbon-intensive process natural gas DRI, with 0.7 tCO2 per tonne of steel.

For one tonne of imported steel HRC, using actual data:

CBAM fees (2026) = (0.7 – (97.5% x 0.481)) x 75.36 = €17.41

CBAM fees (2027) = (0.7 – (95% x 0.481)) x 75.36 = €18.31

CBAM fees (2028) = (0.7 – (90% x* 0.481)) x 75.36 = €20.13

Even for these low-carbon imports, CBAM fees exceed the price paid by EU producers. The above costs do not take into account the cost of switching from the coal-based blast-furnace route to the natural gas DRI route, which is currently less competitive in the EU, even for imports.

The CBAM’s double dividend

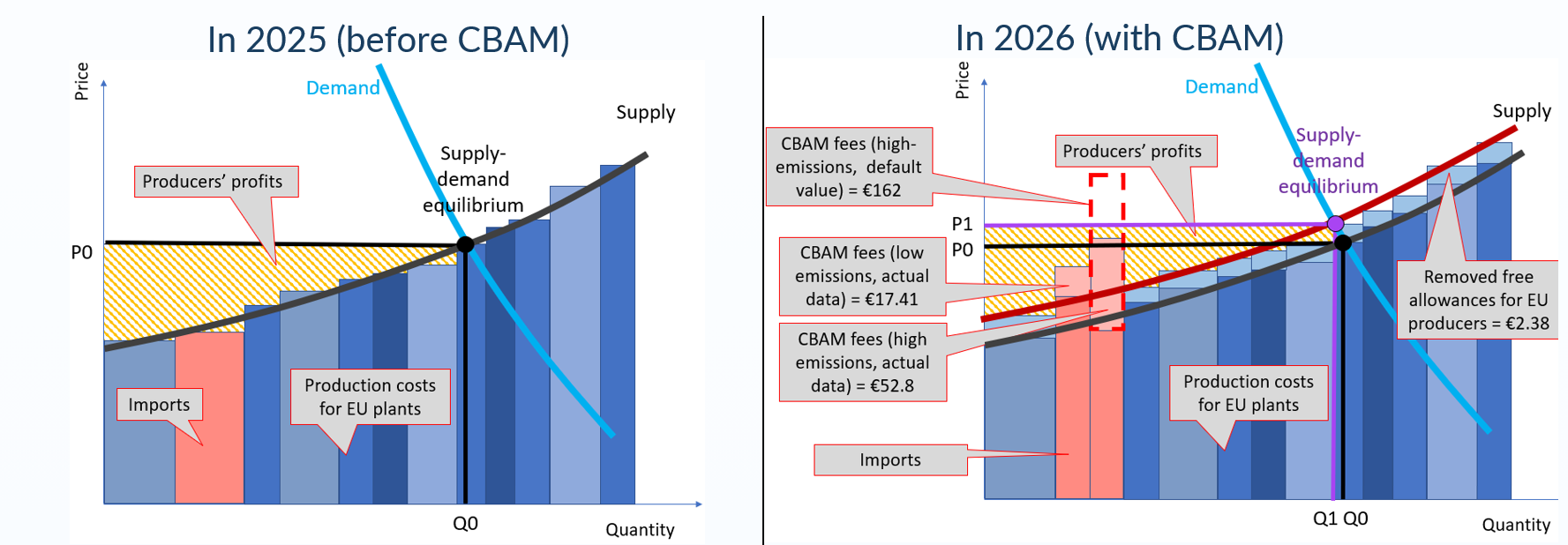

For the first time ever, both EU installations and imports now face carbon costs. However, our calculations show that, at least in the first three years, the balance is favourable to EU installations. This, in turn, will benefit EU producers in terms of competitiveness, as some plants will climb down the cost curve with relatively higher competitiveness than imports, and some imports (e.g. using reporting with default values) will get priced out of the EU market, as illustrated by Figure 1.

Another effect is extra revenues: The addition of carbon costs to all products (EU and foreign) will create an upward shift of the steel HRC supply curve, leading to a higher market price (from P0 to P1 on the picture).

Figure 1: supply-demand curves of steel HRC in 2025 and 2026, including carbon costs for EU installations and imports

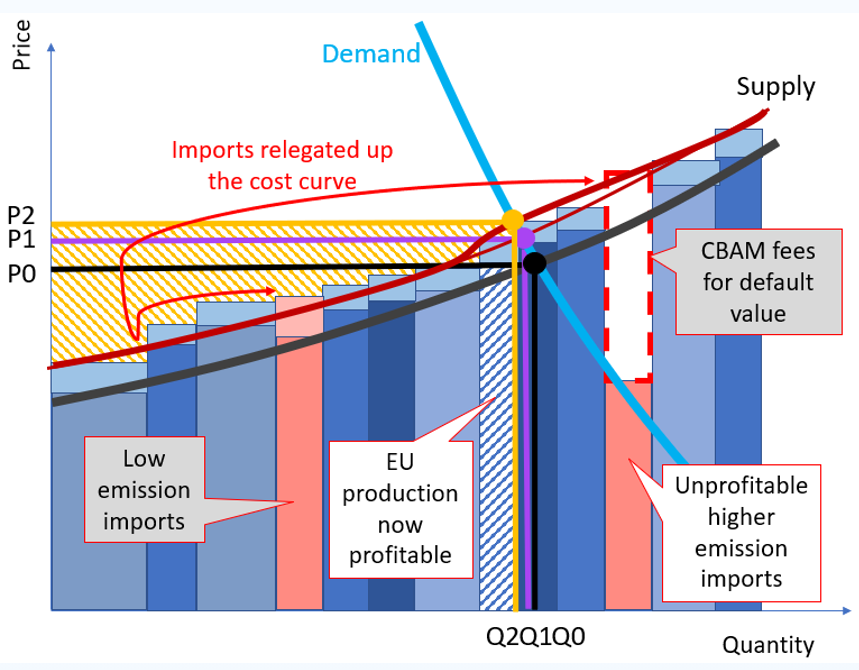

The magnitude of the steel price rise in the EU market is linked to the amount of added ETS costs and the elasticity of steel demand. Given that steel demand is inelastic (people continue to buy it when the price rises, in other words the supply curve is steep), the price rise could get close to 100% of the EU ETS cost increase. But the combined effect of the CBAM is likely to tip that amount above 100%, as some of the cheaper imports are relegated to the high-cost end of the merit order, lifting further up the supply curve and raising the market price further. This is illustrated in Figure 2, where imports that were near the low-cost end of the merit order are relegated to higher-cost parts, including out of the profitable area, whereas previously unprofitable EU production becomes profitable, and the price climbs up again from P1 to P2.

Figure 2: supply demand curve with some imports priced out of the EU market

Icing on the cake: the Innovation Fund

Free allocation and the CBAM’s double dividend are not all the steel sector is receiving. A significant share of ETS allowances are auctioned to feed the Innovation Fund, and as per an amendment of the EU ETS Directive passed in 2023, the Innovation Fund shall “give special attention” to projects in CBAM sectors, when selecting applicants for financing.

According to the European Commission, by the end of 2025, 776 million euros had been spent on iron and steel projects and 2.8 billion euros on hydrogen projects (some of which contribute to the iron and steel industry). This was before the significant uplift in revenues that the Innovation Fund is due to receive from the sale of allowances removed from CBAM sectors. For comparison, the amount of free allocation removed by the CBAM from iron and steel installations in 2026 is only worth about 230 million euros.

Setting priorities right

Despite claims of the contrary, the iron and steel sector benefits from the EU ETS, and this benefit is set to continue for the coming years. With effective measures against circumvention, high default values and administrative burden imposed on importers, the CBAM may be creating conditions for EU producers to earn back the value of their lost free allowances several times over, at least in the first few years of its implementation. If so, giving them more, in the form of subsidies or an extension of free allocation beyond 2034, would procure them an excessive economic rent at the expense of EU consumers and taxpayers.

We are not suggesting here to stop any kind of subsidies to CBAM sectors. These are multiple reasons why projects or sectors might need subsidies, including to face already asymmetrical support in other countries. However, subsidies are not justified as a response or compensation for damages supposedly caused by the EU ETS.

In the longer term, it may happen that firms located in third countries may turn back competition on carbon costs in their favour, by developing cheaper low-carbon steel supply routes to the EU. This might be helped by the CBAM’s current design which rewards the decarbonisation of the relatively small portion of goods that are exported by third countries, regardless of the rest of their production. However, this threat is far from imminent or proven, as low-carbon steel is famously more expensive to produce or source. Moreover, if this happened, changes to the CBAM’s design could be applied to address residual asymmetry. In the meantime, revisiting the schedule of the free allocation phase-out beyond 2028 should be the lowest priority in the EU policy agenda.

Sources:

[1] Financial Times, 15.06.2026, First movers risk losing out in EU green policy pullback; Outokumpu Corporation, 30.06.2026, Joint statement by European steel leaders: Steel businesses for ETS1 and CBAM

[2] ArcelorMittal, 22.06.2026, ArcelorMittal, thyssenkrupp Steel, and voestalpine call for pragmatic ETS reform; POLITICO, 16.06.2026, Vier Stahl- und Chemiekonzerne fordern Einfrieren des ETS

[3] JRC (2023), Greenhouse gas intensities of the steel, fertilisers, aluminium and cement industries in the EU and its main trading partners

[4] For products from countries where the effective carbon price is zero

In the news

Related publications

More on the EU ETS and steel

EU ETS Reform: Let’s not invalidate climate policy!

Based on our updated EU ETS simulator, this technical brief models the impact of the several proposals on the carbon market’s supply/demand balance under the European Commission’s impact assessment emission scenarios.

Improving EU ETS benchmarks: Response to the European Commission’s public consultation on EU ETS benchmarks

Sandbag’s response to the public consultation on the European Commission’s proposed revision of the benchmark values of free allocation of emission allowances (2026-2030).

Rhetoric vs reality: setting the record straight on the impact of the EU ETS on industrial competitiveness

This brief examines whether the claims by Czechia and Italy that the EU ETS is responsible for declining industrial competitiveness hold up to scrutiny.

Don’t Ruin the EU ETS! Joint NGO Letter to the European Council

Ahead of the March European Council meeting, we’ve joined a group of 35 civil society organisations calling on EU leaders to protect the integrity of the EU Emissions Trading System.

Steel labelling: Beyond the sliding scale

As EU policymakers debate how to certify low-carbon steel, Sandbag’s new briefing analyses the “sliding scale” method — and outlines why it may hinder rather than help decarbonisation. A new model is proposed based on product-specific benchmarks, multi-tier ratings, and circularity incentives.

Scrap Steel at Sea: How ship recycling can help decarbonise European steel production

As Europe seeks to decarbonise its steel industry, a new Sandbag report highlights an overlooked solution: high-quality scrap steel from retired ships. With up to 15 million tonnes of certified scrap available annually, ship recycling could meet 20% of EU steel scrap demand — if policy gaps are addressed.

ICC reform and expansion risks diverting ETS revenues from real climate action

Sandbag and 14 other organisations urge the European Commission to reform, not expand, the ETS Indirect Cost Compensation scheme — warning that current proposals risk diverting climate funding into untargeted fossil subsidies.

Sandbag’s feedback to the call for evidence on the Circular Economy Act

Sandbag welcomes the Circular Economy Act (CEA) as an important step to accelerate the transition to a circular economy in the EU. Progress in this area has been slow and this act is sorely needed to address systemic issues holding back circularity, including the current fragmented approaches across Member States.

State Aid for Indirect Carbon Costs: Reform before extending!

Sandbag responds to the EU’s consultation on State aid for Indirect Carbon Costs (ICC), calling for targeted reforms to better support clean electricity, avoid windfall profits, and align with the Carbon Border Adjustment Mechanism (CBAM).

New Principles for Steel Labelling: response to the consultation on the Industrial Decarbonisation Accelerator Act

Sandbag’s response to the EU’s Industrial Decarbonisation Accelerator Act sets out four principles to guide green steel labelling schemes, promoting credible standards based on lifecycle emissions and system-wide decarbonisation.