Based on our updated EU ETS simulator, this technical brief models the impact of the several proposals on the carbon market’s supply/demand balance under the European Commission’s impact assessment emission scenarios.

June 2026

On 1 April 2026, the European Commission published data on the number of free emission allowances in its emissions trading system (EU ETS) and proposed to change its key stabilising mechanism, the market stability reserve (MSR). The European Commission also released preliminary emissions data which shows that stationary installation emissions fell by 1.3% in 2025 from the previous year, and in late May updated supply and demand figures as part of its TNAC [1] communication.

In March this year, ahead of the last Council meeting, the French Environment Minister called for “smoothing the line, so allowances don’t end in 2040 but in 2050” [2]. This was backed by Poland, asking for an annual reduction “from 4.3% towards 2-3%”, [3] and later by Germany, calling for a reduction of the LRF from 2036 onwards,4 referring to the linear reduction factor which sets the emissions cap of the ETS. On various occasions, the European Commission has floated the idea of letting carbon removals and/or international credits into the system, including through “raising the cap”[5]. In early June, EU ETS rapporteur MEP Peter Liese was reported as asking for an LRF at 3.4% [6].

Based on our updated EU ETS simulator, this technical brief models the impact of the above proposals on the market’s supply/demand balance under the European Commission’s impact assessment emission scenarios:

- Emission scenario S1: 75% reduction in EU-wide emissions by 2040 (ETS sectors: -82%)

- Emission scenario S2: 85% reduction in EU-wide emissions by 2040 (ETS sectors: -89%)

- Emission scenario S3: 95% reduction in EU-wide emissions by 2040 (ETS sectors: -93%)

The Impact Assessment provides emission breakdowns between power, industry, aviation, and shipping sectors. We translated these into forecasts for the sectors covered by the EU ETS, drawing linear trajectories from 2025 values to 2040 in the relevant sectors.

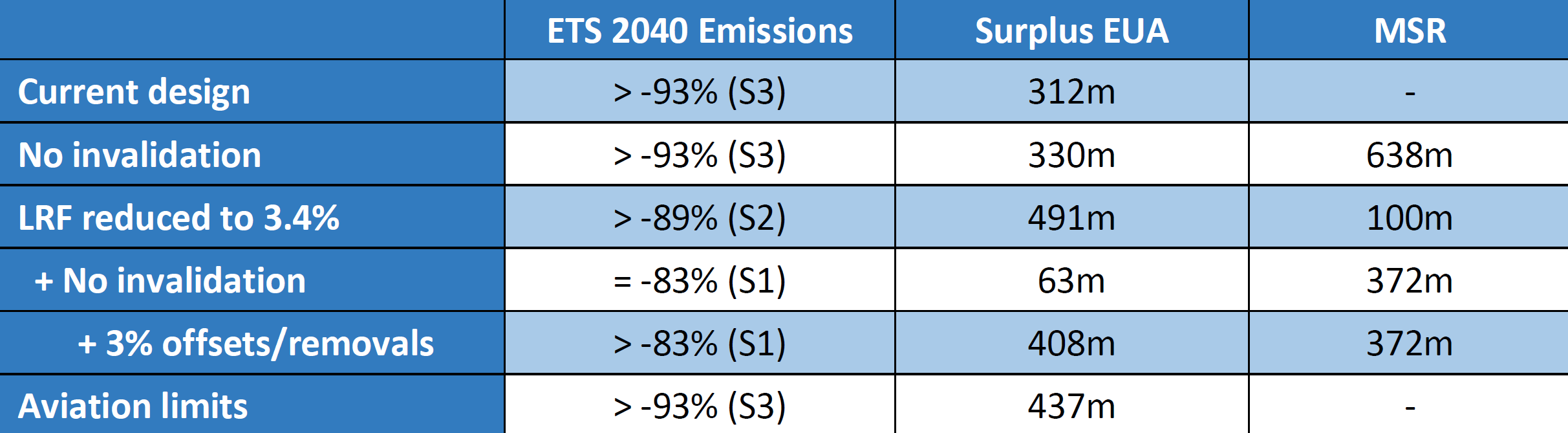

Table 1: Implications of different ETS design options on emissions levels, and surplus EUAs, and the MSR.

Current design

Our first simulation is with the ETS’s current design. Under the current rules, the MSR invalidates allowances when its total exceeds 400m, and the LRF reduces the annual cap by 4.4%, driving it to virtually zero by 2039.

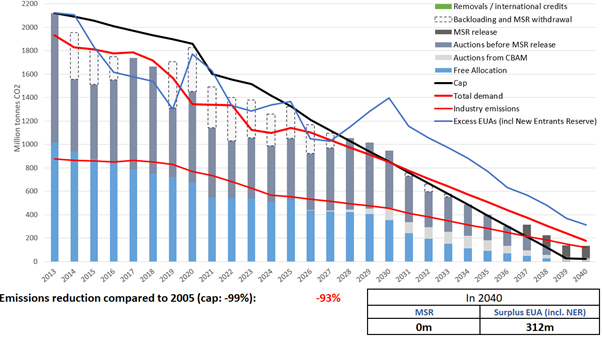

Figure 1 shows the S3 pathway, in which ETS emissions decrease by 93%, with a surplus in the overall market balance of 312m EUAs (in circulation or in the NER, see blue line). The number of allowances in the MSR reaches zero in 2040.

Figure 1: Scenario S3 under the current design of the EU ETS

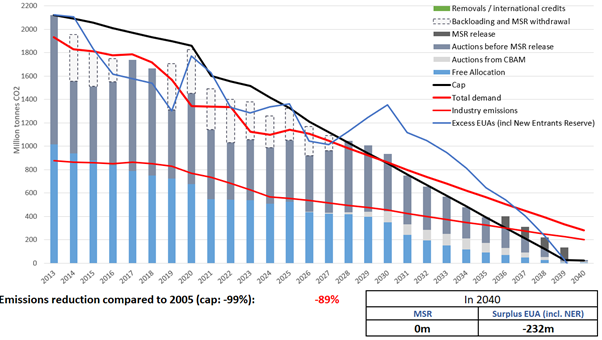

Under the S2 pathway, ETS emissions decrease by only 89%, and the EU as a whole would miss its 90% emissions reduction target. In this scenario, the market has a deficit of -232m EUAs. The market would therefore likely push EUA prices to levels high enough to bring emissions back down and balance the market. The current design effectively drives emissions between scenarios S2 and S3, which is in line the EU’s ambition of climate neutrality by 2050.

Figure 2: Scenario S2 under the current design of the EU ETS

The EU ETS is fit for purpose

Our modelling shows that any of the three reform proposals – suspending the MSR invalidation, reducing the LRF, or introducing removal or offset credits – make this trajectory unattainable. Combining them would be disastrous, driving the carbon price down to levels that would not drive any meaningful decarbonisation.

The EU ETS provides enough allowances to reach the right emission levels by 2040, so the current design is fit for purpose. Weakening it – even a little bit – would have significant negative consequences. To contain prices for industry and raise more funds for alternatives to air transport, we propose to gradually limit the access of airlines to stationary emission allowances.

Footnotes

[1] Total number of allowances in circulation (TNAC).

[2] 20 minutes, La France veut « assouplir » le marché du carbone européen et prolonger les quotas gratuits.

[3] Carbon Pulse, Poland floats slower annual EU ETS emission cuts, targets zero allowances by 2050.

[4] Contexte, ‘Non Paper: Den ETS 1 zukunftsfest machen und die Wettbewerbsfähigkeit stärken’.

[5] Carbon Pulse, ‘Brussels eyes raising EU ETS cap to make room for carbon removals’.

[6] Contexte, ‘ETS veteran Peter Liese rejects far-right alliance for upcoming revision’.

[7] This is less than the TNAC published yearly, which included net aviation demand before 2024.

In the news

Related publications

July 9th 2025

July 8th 2025

July 3rd 2024

More on the EU ETS

Sandbag responds to Thyssenkrupp

Our technical brief on how the ETS is a net benefit for European steelmakers was covered by ESG.Table, alongside a response from Thyssenkrupp Steel, which raised three objections. This response analyses the German steelmaker’s claims.

EU steelmaking: the ETS money is coming!

This brief challenges recent industry claims that EU steelmakers are being harmed by the EU’s Emissions Trading System and finds that the opposite is true.

Improving EU ETS benchmarks: Response to the European Commission’s public consultation on EU ETS benchmarks

Sandbag’s response to the public consultation on the European Commission’s proposed revision of the benchmark values of free allocation of emission allowances (2026-2030).

Rhetoric vs reality: setting the record straight on the impact of the EU ETS on industrial competitiveness

This brief examines whether the claims by Czechia and Italy that the EU ETS is responsible for declining industrial competitiveness hold up to scrutiny.

Don’t Ruin the EU ETS! Joint NGO Letter to the European Council

Ahead of the March European Council meeting, we’ve joined a group of 35 civil society organisations calling on EU leaders to protect the integrity of the EU Emissions Trading System.

ICC reform and expansion risks diverting ETS revenues from real climate action

Sandbag and 14 other organisations urge the European Commission to reform, not expand, the ETS Indirect Cost Compensation scheme — warning that current proposals risk diverting climate funding into untargeted fossil subsidies.

State Aid for Indirect Carbon Costs: Reform before extending!

Sandbag responds to the EU’s consultation on State aid for Indirect Carbon Costs (ICC), calling for targeted reforms to better support clean electricity, avoid windfall profits, and align with the Carbon Border Adjustment Mechanism (CBAM).

Simulating CDR in the EU ETS: The Risks of Premature Integration

Sandbag has developed an ‘ETS + CDR simulator’ to help visualise and explore the impact that CDR integration could have on the ETS, assess the demand it could create for CDR, and highlight the potential consequences of this demand. This report uses the simulator to explore how different integration pathways could affect emissions reductions, carbon prices, and potentially lead to negative externalities.

The EU ETS at a Crossroads

Sandbag’s latest submission to the EU ETS and Innovation Fund consultation calls for clearer rules on free allocation, stronger criteria for funding innovation, and safeguards against misleading carbon accounting practices.

Open letter against international credits integration into the EU 2040 climate target and NDC

A joint NGO letter calls on the EU to exclude international carbon credits from the 2040 target. The signatories urge a domestic-only approach to protect climate credibility and ambition.