Sandbag’s response to the European Commission’s public consultation on the carbon price paid in third countries under the CBAM.

Sandbag welcomes the opportunity to contribute to the public consultation on the European Commission’s proposed implementing regulation (IR), under the CBAM regulation, on the carbon price paid in third countries.

Equivalence with thresholds

According to Recital 8, only carbon prices paid on embedded emissions under a scheme that takes the form of a tax, levy or fee or “imposes compliance obligations on all operators active in the relevant sectors covered by that mechanism without discrimination”.

We believe that this condition should be made more comparable to the EU ETS, which only covers operators above certain thresholds.

Fuel taxes above EU levels

Recital (9) and Article 3.3.3 of Annex I provide that fuel taxes may count towards the effective carbon price. However, for the sake of equal treatment, as fuel taxes applied in the EU do not count towards EU ETS obligations, fuel taxes in third countries should count towards CBAM obligations if they exceed the tax rates applicable in the EU, and only the rate difference between the two jurisdictions (if positive) should count towards the effective price.

Multiple transactions

In the case of an emission trading system, the evidence required by Article 3.5.1 to justify the carbon price paid only takes into account the purchase of compliance units. This fails to capture situations where the units have not only been purchased but also sold, in back-and-forth transactions as is commonly the case with operators covered by the EU ETS.

In such case, the effective price paid should take into account the net number of units purchased (i.e. bought minus sold) and the net cost of all the transactions done by operators.

Revenues recycled into covered installations

A major concern is about revenues from carbon pricing mechanisms (CPM) that are reinjected into the same entities that are covered by them.

The EU CBAM is an opportunity for third countries to benefit from an export market (the EU) with increased selling prices thanks to the inflationary effect of the combined CBAM and phase-out of free allocation in the EU ETS.

Increased revenues (partly or entirely) compensate the acquisition cost of CBAM certificates due at EU borders on the embedded emissions of imported goods. But thanks to the proposed IR, exporting countries may neutralize some of the acquisition costs by setting up carbon pricing mechanisms while still capturing the revenue increase. It is therefore important for the discounts granted in such cases to encourage genuine climate policies in third countries.

The proposed IR states that revenues from CPM that are “reinvested in the decarbonisation of an operator’s installation” should not be considered as compensation for the carbon price paid”, according to Recital 15. Article 8 broadens this exemption to subsidies, whether or not they relate to investments, with only an objective of decarbonisation.

There are however limits in the benefits of recycling carbon revenues into the entities that paid them in the first place, and risk of doing so for the system’s coherence.

Carbon pricing should finance decarbonisation by itself

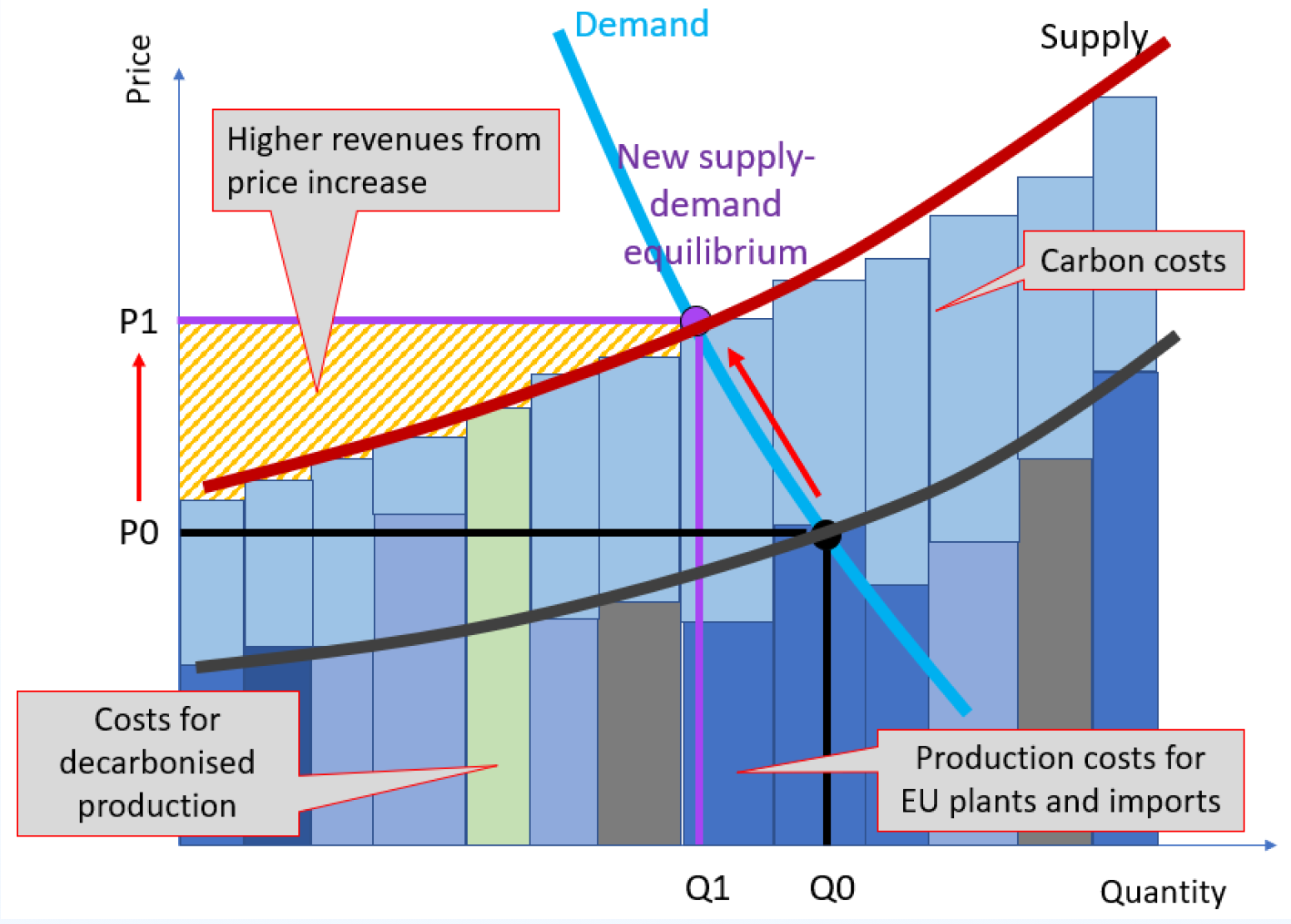

Carbon pricing in the EU, combined with the CBAM, provides its own financing mechanism for decarbonisation, thanks to the pass-through of carbon costs. EU-based operators will be able to pass their carbon costs down value chains through to their customers, thanks to the protection brought by the CBAM from cheaper external competition. This will result in higher market prices, therefore higher revenues for EU producers. The plants that pay for decarbonisation can therefore use those revenues to pay back for these costs (see green rectangle in Figure 1).

The inflationary impact of the CBAM has been widely commented on regarding fertilisers. Even though in 2026 this effect is small because only 2.5% of free allocation is removed, so the effective carbon costs are low under the EU ETS, but it will gradually increase to the benefit of all EU producers. The pass-through of EU carbon costs could even exceed 100% if imports (on average) bear CBAM costs that are higher than EU carbon costs.

There is however a temporary funding gap until full implementation of the CBAM in 2034, where EU market prices of CBAM goods (and the related revenues to producers) will only rise gradually. Subsidies should therefore focus on the period until 2034. In addition, subsidies might be justified in sectors which do not manage to fully pass through their costs, for example due to cheaper competition even with the CBAM in place, but be limited to the fraction of cost that cannot be passed through.

Figure 1: Production costs and carbon costs for EU polluting and decarbonised installations

Subsidising CBAM sectors creates asymmetry

The question of subsidies, with the CBAM, may create asymmetrical situations. This is because, whereas the EU imposes a carbon price on all its installations, only a fraction of the goods produced in third countries are exported to the EU. For example, in 2025, Japan’s steel production was 80.7 million tonnes, and its CBAM-covered steel exports were only 0.8m tonnes (1%) and China produced nearly 1 billion tonnes but only exported 8.9m CBAM steel goods (0.9%) to the EU (Eurostat, Worldsteel).

Only a fraction of EU production can be subsidised, for obvious budgetary reasons, whereas third countries can more easily subsidise all their exports to the EU. We appreciate that paragraph (a), (b) and (c) of Article 8 adds conditions to mitigate this asymmetry, by imposing that all installations covered by the CPM should be eligible to the subsidies and that the decision of the public authority granting the subsidy must be public, but these conditions are too weak.

To ensure fair competition, the decision by the public authority should not only be public but based on criteria that are objective and independent of the CBAM. In addition, to ensure that the discount from CBAM liabilities rewards a subsidy scheme rather than a subsidy paid to an individual installation, it should take into account the coverage of this scheme over total national production.

Controlling where the use and impact of subsidies

Another difficulty concerns controlling the use and impact of subsidies.

Firstly, setting an objective of decarbonisation without evidence of achieving it might turn this condition into a simply administrative formality.

Secondly, it is extremely difficult to know whether a subsidy really serves the purpose it claims to serve. Companies may invest in decarbonisation anyway, because it is sensible for economic or market reasons, so a subsidy earned for decarbonisation might actually be spent on other things – or just increase profits.

Thirdly, specific expenditure should not be considered in isolation from an installation’s broader budget. Typically, companies face various costs, some of which can be see as “decarbonisation” and others doing the opposite. For example, a plant increasing its overall energy use by switching some of its coal use to natural gas (contributing to decarbonisation), but at the same time, also burning more coal in a new unit. Only counting the “decarbonisation” expenditure would be missing the reality of the plant’s operation.

Finally, decarbonisation should be seen at system level rather than at installation level. For example, a subsidy to a hydrogen steel plant might reduce the direct emissions of this plant (leading to lower CBAM fees), while increasing the country’s combustion of coal or gas to meet the extra electricity demand created by the hydrogen steel plant.

In summary, we suggest adding restrictions to Article 8(2), with a view of limiting the spending of EU ETS revenue on CBAM sectors especially after 2034, and provisions to better take into account the scope and impacts of the subsidy schemes eligible for CBAM discounts.

Related publications

April 27th 2026

September 30th 2025

August 6 2024

More on the CBAM

Carbon pricing trends in Asia

This report by Carbon Market Watch, with analysis by Sandbag, examines potential CBAM costs for Japan, South Korea, Vietnam, Indonesia, and the Philippines, based on their trade exposure, production outlooks, and progress toward implementing a domestic carbon price signal.

An opt-in solution to CBAM circumvention and complexity

Our position paper on the Commission’s legislative proposal amending the CBAM proposes an opt-in solution to CBAM circumvention and complexity.

The EU CBAM gives a boost to Algeria’s iron exports

Sandbag’s brief assesses how the EU Carbon Border Adjustment Mechanism (CBAM) may affect Algeria’s iron and steel exports. It finds that although Algeria’s overall exposure to CBAM is limited, rising EU carbon costs are likely to increase EU market prices, with implications for the revenues and competitiveness of Algerian exports.

CBAM and Fertiliser Inflation in 2026: The facts behind the numbers

Estimates suggesting that the EU’s Carbon Border Adjustment Mechanism (CBAM) could increase fertiliser prices by up to 30% have brought a central question into focus: how significant is the inflationary impact likely to be?

The CBAM dividend for Namibia and Ghana

This research note shows that Namibia and Ghana are likely to benefit from the CBAM, as EU price increases linked to the EU ETS outweigh CBAM fees under current exports. It also sets out transparent transformation scenarios, based on announced industrial projects, to show how expanded and lower-emissions production could further increase export revenues over time.

Chemicals in the CBAM: Time to step up

Sandbag’s latest brief explains why the EU CBAM must be expanded to cover key chemical value chains. With chemicals and refinery products responsible for 30% of industry emissions, phased inclusion is critical to prevent carbon leakage and phase out free allowances.

The EU CBAM: a two-way street between the EU and Africa

The Carbon Border Adjustment Mechanism CBAM is often misunderstood as a trade policy whereas it is actually a climate policy. Its only objective, as stated in Article 1 of the CBAM Regulation, is to replace the current system of free allocation of emission allowances to EU-based manufacturers under the EU carbon market.

Sandbag’s Response to the CBAM Calls for Evidence

Sandbag has submitted responses to the EU’s CBAM calls for evidence, addressing emissions reporting, adjustment for free allocation, and carbon prices paid abroad. We highlight risks such as loopholes and unequal treatment, and propose practical solutions to strengthen CBAM’s effectiveness and fairness.

CBAM impact on US trade: an analysis

Sandbag’s September 2025 research note explores the impact of the EU’s CBAM on US exports. It finds that even with expanded scope, the financial impact remains marginal, and US carbon pricing could turn net costs negative.

The EU CBAM: A Two-Way Street to Climate Integrity?

Supported by the Konrad-Adenauer-Stiftung, Sandbag’s report examines the impact of the EU’s Carbon Border Adjustment Mechanism (CBAM) and the gradual removal of free allowances on third-country exporters. The joint implementation is expected to raise production costs for both EU and non-EU producers, leading to higher prices for CBAM-covered goods in the EU.