Industry decarbonisation

We explore the potential of electrification, circularity, and other technologies to decarbonise energy-intensive sectors like steel, aluminium, and cement.

About industry decarbonisation

Decarbonising heavy industies is key to achieving the EU's net-zero target by 2050

Heavy industries (e.g. chemicals, steel, cement, non-ferrous metals, …) are used in sectors such as construction, transport and agriculture. These industries are amongst the biggest emitters.

Decarbonisation policies and solutions need to be improved and developed to make progress

- EU policies, such as the EU Emissions Trading System (ETS), should better incentivise decarbonisation.

- Electrification, substitutions, and circularity are obvious solutions to decarbonise industry.

- In some cases, other technologies such as hydrogen and carbon capture, utilisation and storage (CCUS) may be useful.

Our work

Conducting research

We analyse the potential of electrification, circularity, and other technologies such as hydrogen and CCUS.

We aim to identify actionable pathways and policy solutions to decarbonise heavy industries.

Evidence-based advocacy

We actively advocate for our data-driven and evidence-based policy recommendations through:

- Expert groups and alliances: We are part the Commission’s Climate Change Policy Expert Group (CCEG) on the Free Allocation Regulation, Carbon Border Adjustment Mechanism (CBAM) expert group for DG CLIMA and DG TAXUD, and DG GROW’s Clean Hydrogen Alliance.

- Collaboration: We collaborate with climate organisations around campaigns.

- Policy recommendations: We provide direct feedback to institutions through public and private outreach.

Read our analysis and policy recommendations

Getting Electrification Right: The broader challenge of induced emissions

Sandbag’s latest report explores how the climate impact of electricity use depends not just on how it’s generated, but also when and where it’s consumed. Using hydrogen as a case study, the report shows how poorly timed renewable electricity use can unintentionally drive-up fossil fuel emissions — and outlines smarter paths to decarbonisation.

Steel emissions standards under threat from flawed “mass balance” proposal

A joint letter from 30+ NGOs warns that coal-based steel could be falsely labelled as green under proposed “mass balance” rules. The signatories call for traceable, credible emissions data in steel standards.

Joint statement urges EU to boost the use of recycled steel scrap in the automotive sector

A new joint statement urges the EU to set binding targets for recycled steel use in cars, citing the climate benefits of secondary steel and the need to reduce demand for high-emission imports.

Developing data tools

We develop data tools to analyse industrial emissions and to assess different technologies.

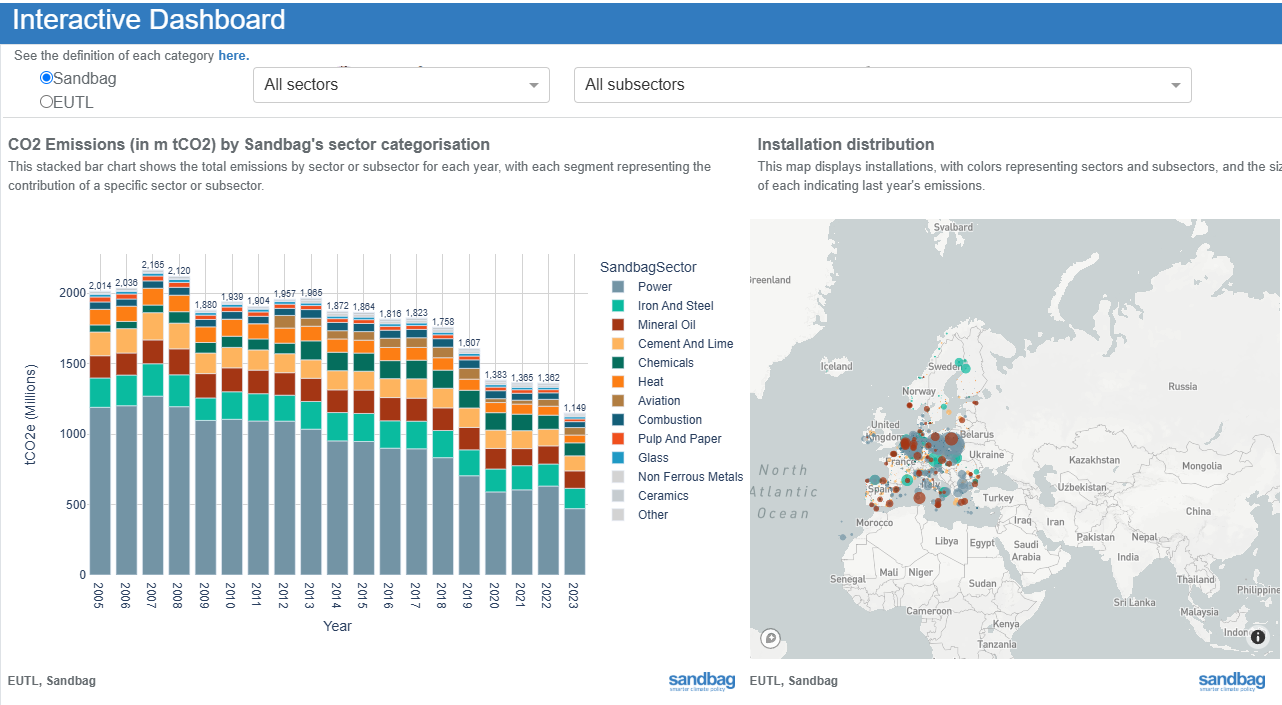

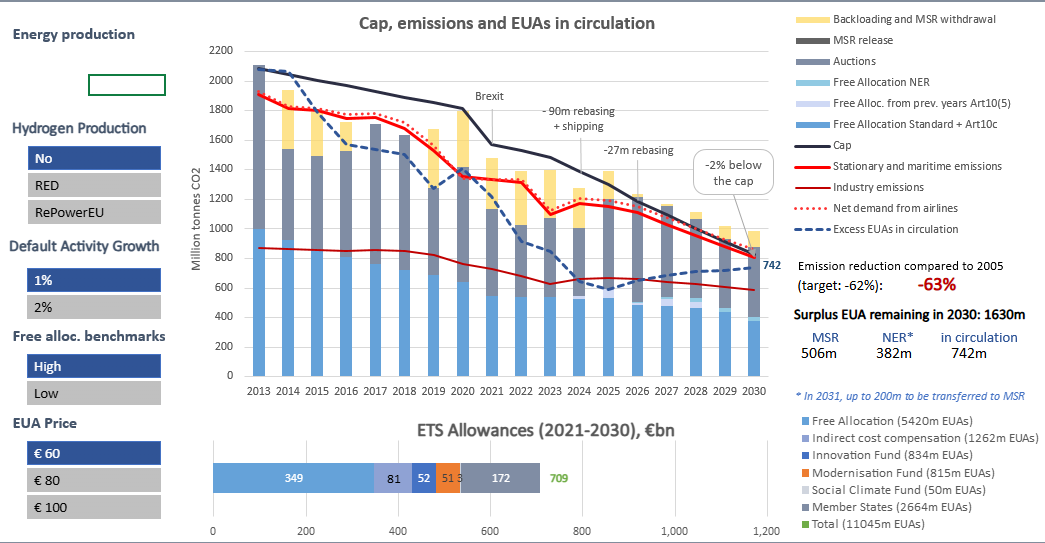

EU ETS Dashboard

Navigate emissions data of sectors covered by the EU ETS at various granularity levels.

Marginal Abatement Cost (MAC) Curve

Assess when switching to renewable hydrogen becomes cost-effective for refining, methanol, and ammonia production.

Our messages

On steel

- Free allocation in the EU ETS should be phased out.

- Before this is done, free allocation should be done in equal amounts for a given type of product (long or flat) regardless of feedstock and production route

- Carbon Border Adjustment Mechanism (CBAM) should attribute embedded emissions to steel scrap to prevent circumvention.

On hydrogen

- Avoid unnecessary demand for green hydrogen in sectors with better alternatives.

- Distribute aid fairly across competing solutions, prioritising low-carbon, resource-efficient alternatives like recycling and organic fertilisers.v

- Reform EU criteria for green hydrogen to prevent overreliance on fossil fuels and price volatility.

Get involved and support us towards this effort!

We need to improve decarbonisation policies and develop solutions to achieve the EU’s net-zero targets by 2050.

WHAT WE DO

TOOLS

PUBLICATIONS

NEWSLETTER

Mundo-b Matogné. Rue d’Edimbourg 26, Ixelles 1050 Belgium.

Sandbag is a not-for-profit (ASBL) organisation registered in Belgium under the number 0707.935.890.

EU transparency register no. 277895137794-73.

VAT: BE0707935890.