The EU's Carbon Market (EU ETS)

EU Climate Ambition is Under Threat

What is the EU Emissions Trading System (EU ETS)?

The EU ETS is the European Union’s flagship climate policy.

Under a cap-and-trade system, the EU issues a limited number of pollution rights (EU Emissions Allowances). This number decreases each year, creating an increasingly scarce and expensive asset that incentivises decarbonisation.

Carbon intensity in the sectors covered by the EU ETS has already decreased by 62% since 2005, mostly in the power sector.

Other sectors receive free emission rights, which dampens the financial incentive to decarbonise. However, thanks to the EU’s Carbon Border Adjustment Mechanism (CBAM), free emissions allowances will be phased out.

Source: European Environment Agency – Greenhouse gas emissions under the EU Emissions Trading System

Yet, the EU ETS is facing growing political pressure. Proposals from politicians and industry groups to weaken or even suspend the ETS, as well as to delay the phase-out of free allowances, risk undermining investor confidence, slowing decarbonisation, increasing reliance on imported fossil fuels and raw materials, and reducing public revenues from auctions of emission permits.

This comes at a time when policy stability is essential to deliver Europe’s climate and competitiveness goals. If the objective is to address competitiveness, the solution lies in using and improving the existing system and not in weakening it.

Frequent EU ETS Questions

Is the EU ETS responsible for the EU's loss of competitiveness?

No. Companies in energy-intensive trade-exposed sectors — steel, cement, chemicals — receive free EU Allowances to mitigate the carbon leakage risk.

Because of the large proportion of free allowances (covering nearly 100% of emissions on average, even more for some companies), the effective carbon cost has been very low, and has sometimes even been negative.

The ETS is therefore not responsible for losses of competitiveness in the EU.

Does the EU ETS increase electricity prices?

Yes, it has a modest effect — but industrial users are generously compensated.

A provision of the EU ETS called “indirect cost compensation” allows Member States to compensate those costs. Italy, for instance, can reimburse industry an amount equivalent to 368 kg CO₂ per MWh consumed — what is comparable to most gas-fired power plants emissions.

The system even allows for providing compensation, if the price paid is lower than the actual carbon cost incurred.

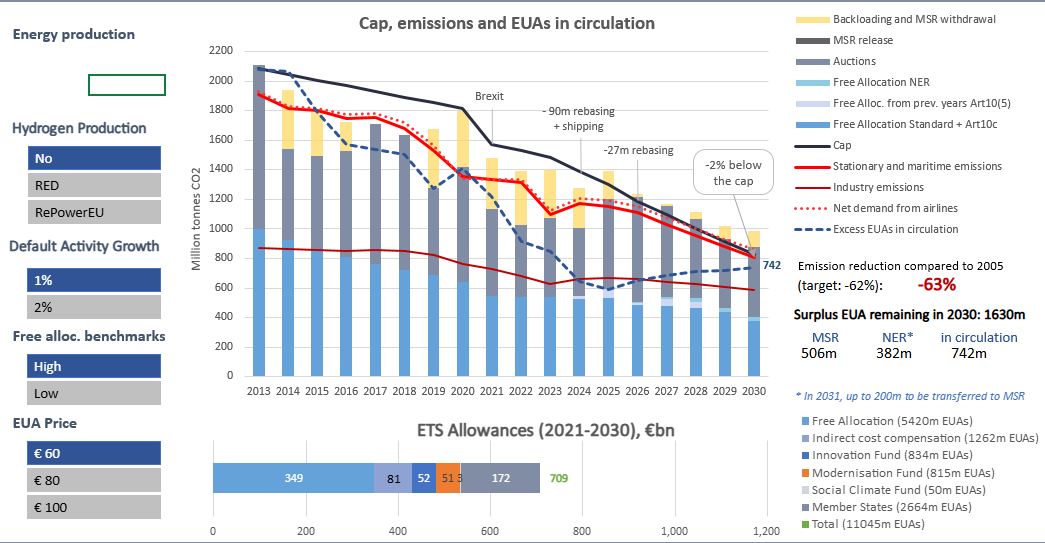

Will the EU ETS bring emissions down to zero by 2039?

No. The large surplus of unallocated allowances in the system means emissions do not have to reach zero by 2039.

Sandbag’s modelling shows that even if emissions fall by around 80% from 2025 levels by 2040, there would still be enough surplus to cover a full year of emissions.

The cap is less stringent in practice than it appears — making proposals to weaken it even harder to justify.

How to Improve the EU ETS

Keep the EU ETS cap

The EU ETS cap is not as stringent as it seems. Despite a trajectory going down to near zero by 2039, a large residual surplus of allowances accumulated in the system would ensure compliance even with moderate emission reductions.

Restrict access to EUAs for airlines

Access to stationary EU Allowances (EUAs) should be restricted for airlines. This would better reflect the different exposures between airlines and industry to international competition, increase the price of aviation allowances (EUAAs), make sustainable fuels more competitive, reduce demand for air transport and raise financing for rail infrastructure.

Incentivise Renewable Electricity

Compensation for indirect carbon cost (for large electricity consumers) is not sustainable. It should be reformed to better incentivise the use of renewable electricity and be compatible with the CBAM.

No carbon credits in the EU ETS

Carbon credits (offsets) or carbon dioxide removals are not necessary to meet the 2040 cap and should be kept out of the system until then.

Phase out free allocation

Free allocation of allowances is a major obstacle to decarbonisation and should be phased out as soon as possible and replaced by the CBAM as protection against carbon leakage (i.e. unfair competition from countries with low or no carbon pricing). While it’s still in place, free allocation should be reformed from process-based to product-based, similar to CBAM benchmarks.

Reform the innovation fund

The Innovation Fund should be reformed. Instead of providing grants for projects without technology risk, it should only give grants to cover technology risk, otherwise only provide performance-based funding. It should promote alternatives to CBAM-covered products instead of subsidise those same sectors already protected by the CBAM

Our Work

Our research and policy recommendations: We closely monitor political developments around the EU ETS, analyse legislative proposals and design options using proprietary simulation models, and we create technical briefs, research notes, and evidence-based policy recommendations to improve the EU ETS.

EU ETS Reform: Let’s not invalidate climate policy!

Based on our updated EU ETS simulator, this technical brief models the impact of the several proposals on the carbon market’s supply/demand balance under the European Commission’s impact assessment emission scenarios.

Rhetoric vs reality: setting the record straight on the impact of the EU ETS on industrial competitiveness

This brief examines whether the claims by Czechia and Italy that the EU ETS is responsible for declining industrial competitiveness hold up to scrutiny.

Simulating CDR in the EU ETS: The Risks of Premature Integration

Sandbag has developed an ‘ETS + CDR simulator’ to help visualise and explore the impact that CDR integration could have on the ETS, assess the demand it could create for CDR, and highlight the potential consequences of this demand. This report uses the simulator to explore how different integration pathways could affect emissions reductions, carbon prices, and potentially lead to negative externalities.

The EU ETS at a Crossroads

Sandbag’s latest submission to the EU ETS and Innovation Fund consultation calls for clearer rules on free allocation, stronger criteria for funding innovation, and safeguards against misleading carbon accounting practices.

In or Out: What’s best for carbon removals and the EU ETS?

What will the future of the EU Emissions Trading System (ETS) look like as the emissions cap heads towards zero? Is integrating carbon dioxide removals (CDRs) into the ETS a solution to help the EU achieve its climate goals? Or would they compromise the integrity and functioning of the system? These questions are at the forefront of the Commission’s mind as they review different options for the future of the ETS ahead of the 2026 revision.

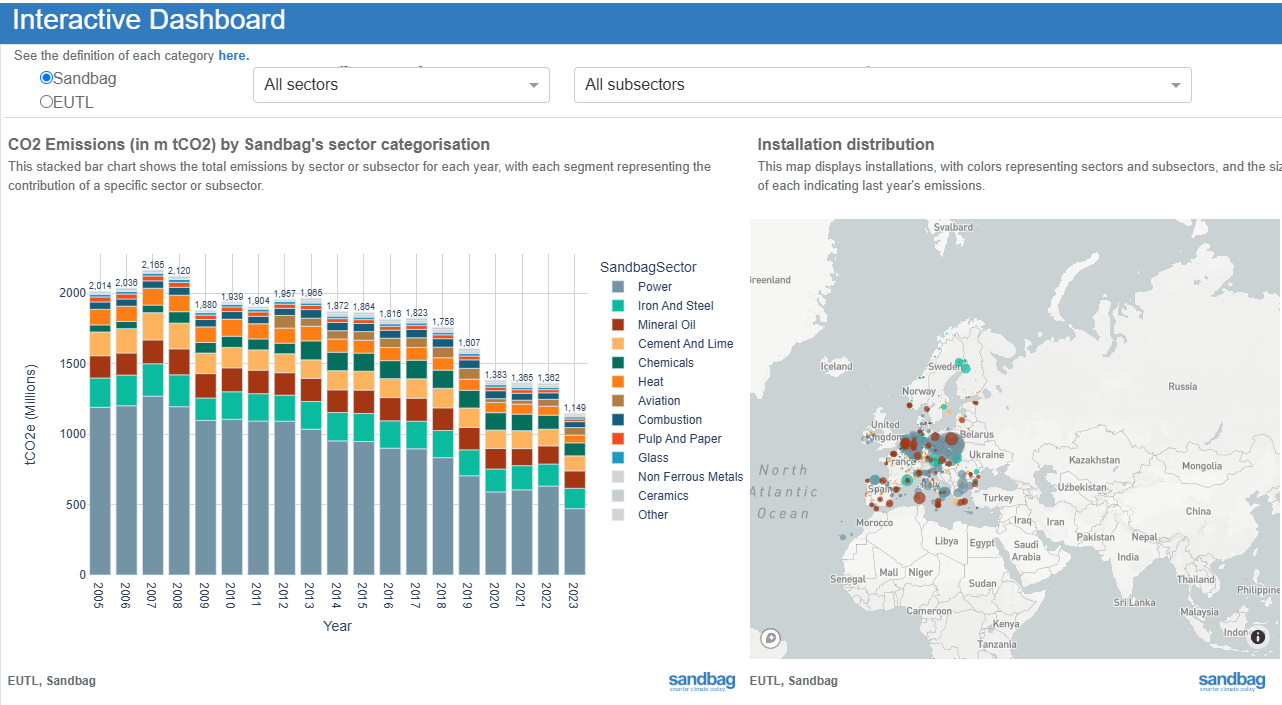

A closer look at 2023 emissions: steelmaking caused a quarter of industry pollution

This brief analyses 2023 emissions under the EU Emissions Trading System (EU ETS), using the latest data available from the EU Transaction Log (EUTL) . It particularly focuses on the iron and steel sector.

Feedback on the inclusion of permanent CCU in the EU ETS

Sandbag urges strict safeguards on permanent CCU within the EU ETS, calling for clear permanence standards, transparent product reviews, and faster removal of free allowances, while stressing CCU must complement (not replace) direct emission reductions.

Supply and demand in the EU ETS: It’s the hydrogen, stupid!

Learn about the supply and demand balance of the EU ETS through the end of its fourth phase in 2030, based on the latest market data and policy parameters. Are the results aligned with the EU’s target of a 55% reduction in emissions?

Joint letter calling for separate emissions reductions and permanent CDR targets in EU 2040 climate framework

Sandbag co-signed an open letter sent to the European Commission by 114 leading academics, businesses, civil society organisations and research institutions urging the EU to set explicit and separate targets for greenhouse gas emissions reductions, land-based carbon...

Update of the EU ETS free allocation rules: Polluting for free during a climate crisis

In this joint op-ed, first featured in Carbon Pulse, Sandbag policy officer Aymeric Amand and Carbon Market Watch policy expert Lidia Tamellini examine the revision of the Free Allocation Regulation. The EU Emissions Trading System (ETS) is one of the core EU...

How we help shape policy: We contribute to several European Commission Expert Groups, respond to public consultations and calls for evidence, and engage directly with policymakers at the EU Commission, EU Parliament, and Member State level. We initiate and join coalition actions with civil society and private stakeholders, speak at public events, and raise awareness through media and social media.

Improving EU ETS benchmarks: Response to the European Commission’s public consultation on EU ETS benchmarks

Sandbag’s response to the public consultation on the European Commission’s proposed revision of the benchmark values of free allocation of emission allowances (2026-2030).

Don’t Ruin the EU ETS! Joint NGO Letter to the European Council

Ahead of the March European Council meeting, we’ve joined a group of 35 civil society organisations calling on EU leaders to protect the integrity of the EU Emissions Trading System.

ICC reform and expansion risks diverting ETS revenues from real climate action

Sandbag and 14 other organisations urge the European Commission to reform, not expand, the ETS Indirect Cost Compensation scheme — warning that current proposals risk diverting climate funding into untargeted fossil subsidies.

State Aid for Indirect Carbon Costs: Reform before extending!

Sandbag responds to the EU’s consultation on State aid for Indirect Carbon Costs (ICC), calling for targeted reforms to better support clean electricity, avoid windfall profits, and align with the Carbon Border Adjustment Mechanism (CBAM).

The EU ETS at a Crossroads

Sandbag’s latest submission to the EU ETS and Innovation Fund consultation calls for clearer rules on free allocation, stronger criteria for funding innovation, and safeguards against misleading carbon accounting practices.

Our interactive tools: We have created and published the EU ETS Dashboard and the EU ETS Simulator to help policymakers and stakeholders understand the state of the EU ETS and impacts of various policy design options.

Get involved and support us towards this effort!

While these developments mark important progress, we need more profound changes for the EU ETS to effectively drive decarbonisation at the scale and pace required.

Mundo Matogné. Rue d’Edimbourg 26, Ixelles 1050 Belgium. Sandbag is a not-for-profit (ASBL) organisation registered in Belgium under the number 0707.935.890. EU transparancy register no. 277895137794-73. VAT: BE0707935890