Carbon Border Adjustment Mechanism (CBAM)

Adjusting carbon pricing between the EU and third countries

What is the CBAM?

The CBAM is an important climate policy that enables the phase out of free allocation of emission allowances under the EU Emissions Trading System (EU ETS). The CBAM places a carbon price on imports of specific goods entering the EU, with CBAM certificates sold at a price that mirrors the carbon costs that EU producers bear under the EU ETS.

However, EU industrial sectors have been receiving free emission permits under the EU ETS, to protect them against international competition. This has reduced their incentive to decarbonise. Phasing in the CBAM and phasing out free allocation will therefore create the conditions to decarbonise EU industry. At the same time, it is expedted to encourage decarbonisation outside of the EU.

The CBAM is facing challenges from both within and outside of the EU.

Outside of the EU, the CBAM has been criticised as protectionist, unilateral, unfair, and even colonialist.

Within the EU, some industries have asked to keep free allocation under the EU ETS – which would significantly reduce the measure’s environmental benefit. Some EU Member States, key Members of the European Parliament and key Commissioners have echoed these calls.

Frequent CBAM Questions

Is the CBAM a protectionist measure?

No. The CBAM only applies to a small number of specifically emission-intensive products, and is designed to mirror the carbon costs that EU producers bear under the EU ETS. Rather than shielding EU industry from competition, it ensures that imported and domestic goods face equivalent carbon pricing, levelling the playing field.

Should the CBAM not apply a higher constraint on the EU than on lower-income countries, in line with the UN’s Common but Differentiated Responsibility principle (CBDR)?

The CBAM does not currently apply differentiated treatment based on countries’ development status. However, the EU argues that its design is consistent with CBDR: Through the EU ETS and the EU’s commitment to reduce emissions by 55% by 2030 compared to 1990 levels, the EU imposes a high carbon constraint on itself. Lower-income countries, by contrast, face CBAM fees only on goods they choose to export to the EU and can reduce or eliminate those fees in different ways (e.g. see below).

Does the CBAM make the EU richer at the expense of third countries?

Not by design. Because the CBAM and EU ETS raise carbon costs for all affected goods sold in the EU regardless of origin, it shifts the market price upward for everyone. While third-country producers face a CBAM fee, they also benefit from this higher market price on the goods sold — including if their CBAM costs are lower than the price rise in the EU market. This can generate windfall profits that exceed the CBAM cost, meaning that some third-country producers may even benefit financially from the CBAM.

Beyond this, third countries that introduce equivalent carbon pricing can reduce their CBAM cost and retain those revenues domestically, rather than seeing them flow to the EU budget.

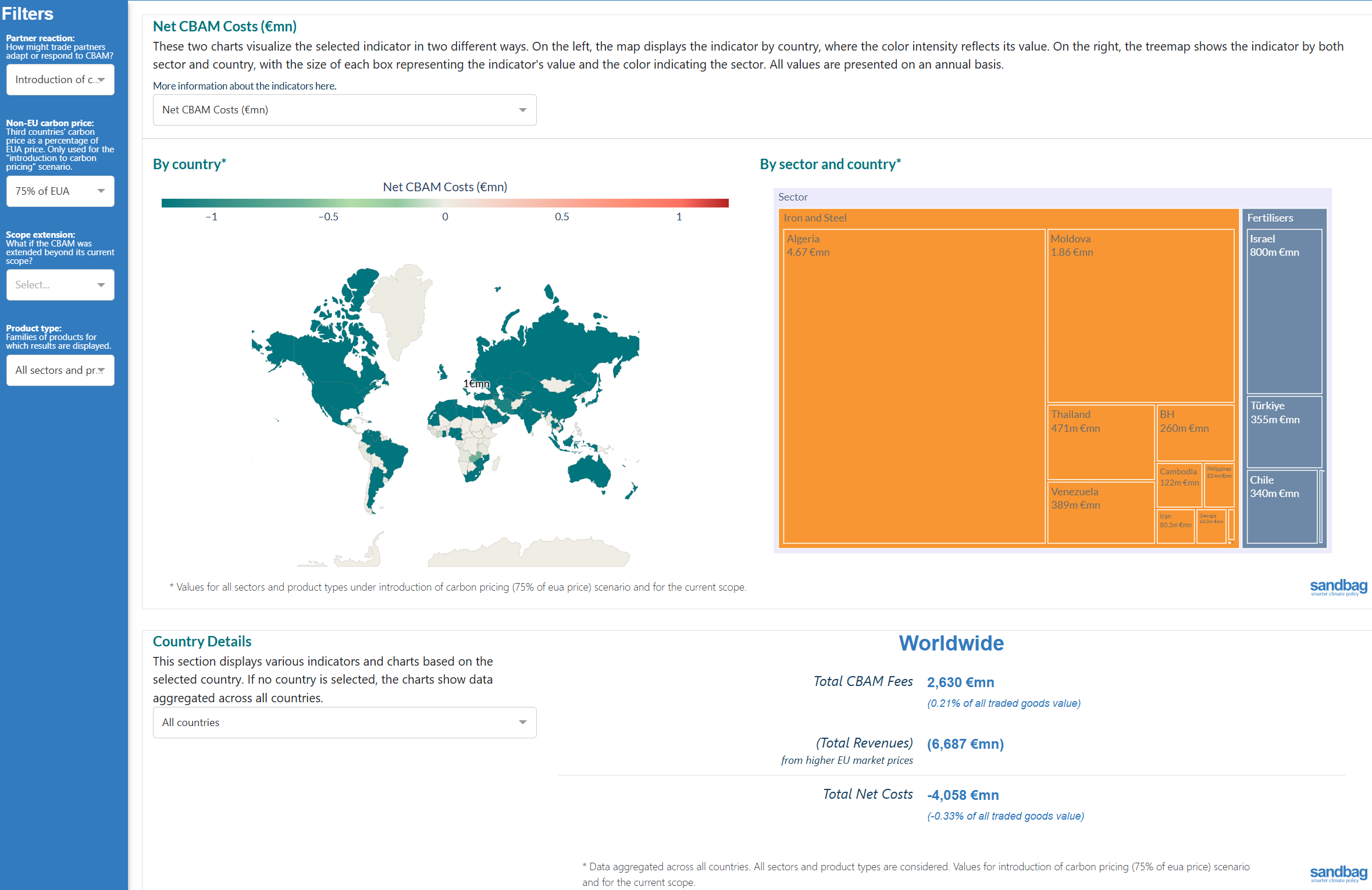

Please try our CBAM Simulator to check the policy’s impacts at country, sector or even product level!

Is the CBAM responsible for fertiliser price increases?

Not significantly in the short term. As we have shown, the impact of the CBAM on fertiliser prices in the EU will be low in the early years of implementation. Temporarily excluding fertilisers from the scope as a short-term relief against high fossil fuel prices would not shift the needle on this, and would undermine progressive business cases in the EU.

In the longer run, the CBAM will increase the market price of fertilisers in the EU, which is why we proposed that the European Commission should assess the possible extension of the CBAM to some agricultural imports.

How to Improve the CBAM

Avoid circumvention incentives and accelerate the phase out free allocation under the EU ETS

One measure could be attributing emissions to aluminium and steel scrap.

Emissions reporting could be based on default values more systematically, i.e. attributing the same emission intensity to all products of the same type manufactured in a given country, based on the country average. To secure cooperation from third countries, the systematic use of default values could apply based on an opt-in basis (at country level) and rewarded by lower default values, reflective of country averages (with no mark-ups) rather than punitive ones. The benefits thereof and a possible amendment can be found in this position paper.

Extend the CBAM’s emission coverage

We recommend including indirect emissions from the use of electricity, for example in the steel sector, where steel imports made from electrolytic hydrogen is currently considered as zero-emissions even if coming from countries with high-emission electricity.

We also recommend including emissions from inputs of CBAM goods such as coke, lime, alumina and pre-bake anode, to phase out free allocation to these inputs in the EU.

More sectors, such as organic chemicals, refinery products and polymers, should be covered by the CBAM to allow for phasing out more free allowances under the EU ETS.

Extend down value chains as appropriate

The CBAM is unlikely to drive significant price rises in the EU in the first few years, but it will in the long run, when free allocation will have been reduced significantly. To avoid negative effects on goods made in Europe, the EU should assess downstream extensions including in sectors such as agricultural goods, where the use of imported fertilisers could be given an unfair competitive advantage compared to EU-made products.

Our Work

Our research and policy recommendations: We closely monitor political developments around the CBAM, analyse legislative proposals and design options using proprietary simulation models, and we create technical briefs, research notes, and evidence-based policy recommendations to improve the CBAM.

Carbon pricing trends in Asia

This report by Carbon Market Watch, with analysis by Sandbag, examines potential CBAM costs for Japan, South Korea, Vietnam, Indonesia, and the Philippines, based on their trade exposure, production outlooks, and progress toward implementing a domestic carbon price signal.

The EU CBAM gives a boost to Algeria’s iron exports

Sandbag’s brief assesses how the EU Carbon Border Adjustment Mechanism (CBAM) may affect Algeria’s iron and steel exports. It finds that although Algeria’s overall exposure to CBAM is limited, rising EU carbon costs are likely to increase EU market prices, with implications for the revenues and competitiveness of Algerian exports.

CBAM and Fertiliser Inflation in 2026: The facts behind the numbers

Estimates suggesting that the EU’s Carbon Border Adjustment Mechanism (CBAM) could increase fertiliser prices by up to 30% have brought a central question into focus: how significant is the inflationary impact likely to be?

The CBAM dividend for Namibia and Ghana

This research note shows that Namibia and Ghana are likely to benefit from the CBAM, as EU price increases linked to the EU ETS outweigh CBAM fees under current exports. It also sets out transparent transformation scenarios, based on announced industrial projects, to show how expanded and lower-emissions production could further increase export revenues over time.

Chemicals in the CBAM: Time to step up

Sandbag’s latest brief explains why the EU CBAM must be expanded to cover key chemical value chains. With chemicals and refinery products responsible for 30% of industry emissions, phased inclusion is critical to prevent carbon leakage and phase out free allowances.

The EU CBAM: a two-way street between the EU and Africa

The Carbon Border Adjustment Mechanism CBAM is often misunderstood as a trade policy whereas it is actually a climate policy. Its only objective, as stated in Article 1 of the CBAM Regulation, is to replace the current system of free allocation of emission allowances to EU-based manufacturers under the EU carbon market.

CBAM impact on US trade: an analysis

Sandbag’s September 2025 research note explores the impact of the EU’s CBAM on US exports. It finds that even with expanded scope, the financial impact remains marginal, and US carbon pricing could turn net costs negative.

The EU CBAM: A Two-Way Street to Climate Integrity?

Supported by the Konrad-Adenauer-Stiftung, Sandbag’s report examines the impact of the EU’s Carbon Border Adjustment Mechanism (CBAM) and the gradual removal of free allowances on third-country exporters. The joint implementation is expected to raise production costs for both EU and non-EU producers, leading to higher prices for CBAM-covered goods in the EU.

Closing the CBAM scrap loophole – A critical move for climate & competitiveness

This joint op-ed by Norsk Hydro, Alcoa, Bellona Europe and Sandbag was published by Carbon Pulse. The EU’s Carbon Border Adjustment Mechanism (CBAM) was established to extend Europe’s carbon pricing to imported products, aiming to create a level playing field between...

A Scrap Game: Impacts of the EU Carbon Border Adjustment Mechanism

Currently, we are in the CBAM transitional period, with negotiations ongoing for its full implementation in January 2026. Learn about the legislative process and the effect of this policy on the EU’s main trade partners, especially China.

How we help shape policy: We contribute to the European Commission’s CBAM Expert Group, respond to public consultations and calls for evidence, and engage directly with policymakers at the EU Commission, EU Parliament, and Member State level. We initiate and join coalition actions with civil society and private stakeholders, speak at public events, and raise awareness through media and social media.

Whether the carbon price is right: response to the European Commission’s public consultation on carbon price paid in third countries

Sandbag’s response to the European Commission’s public consultation on the carbon price paid in third countries under the CBAM.

An opt-in solution to CBAM circumvention and complexity

Our position paper on the Commission’s legislative proposal amending the CBAM proposes an opt-in solution to CBAM circumvention and complexity.

The EU CBAM gives a boost to Algeria’s iron exports

Sandbag’s brief assesses how the EU Carbon Border Adjustment Mechanism (CBAM) may affect Algeria’s iron and steel exports. It finds that although Algeria’s overall exposure to CBAM is limited, rising EU carbon costs are likely to increase EU market prices, with implications for the revenues and competitiveness of Algerian exports.

Sandbag’s Response to the CBAM Calls for Evidence

Sandbag has submitted responses to the EU’s CBAM calls for evidence, addressing emissions reporting, adjustment for free allocation, and carbon prices paid abroad. We highlight risks such as loopholes and unequal treatment, and propose practical solutions to strengthen CBAM’s effectiveness and fairness.

Strengthening the CBAM — by default

The consultation aims to address concerns that the CBAM has loopholes that could distort competition between products manufactured in the EU (covered by the EU ETS) and imported goods. Our response sets out proposals for how the design of the CBAM could be improved in these regards.

Extending the CBAM to indirect emissions

The European Commission is considering amending the Carbon Border Adjustment Mechanism (CBAM) to include indirect emissions of CO2 from the use of electricity in the manufacturing of CBAM-covered goods.

CBAM extension: Closing the emissions gap

Free allocation has long been used to address carbon leakage under the EU ETS, but it has key limitations. It only covers emissions up to benchmark levels, fails to reward cleaner EU producers, and forfeits auction revenues that could support decarbonisation. It also creates perverse incentives by making high-emission goods artificially cheap.

Our interactive tools: We have created and published the CBAM Simulator to help policymakers and stakeholders understand the state of the CBAM and impacts of various policy design options.

Get involved and support us towards this effort!

While these developments mark important progress, we need more profound changes for the EU ETS to effectively drive decarbonisation at the scale and pace required.

Mundo Matogné. Rue d’Edimbourg 26, Ixelles 1050 Belgium. Sandbag is a not-for-profit (ASBL) organisation registered in Belgium under the number 0707.935.890. EU transparancy register no. 277895137794-73. VAT: BE0707935890